Among all the information flying out of these hearings has been one chart that demonstrates AKLNG’s fundamental weakness. Consultants Gaffney Cline presented a “Breakeven Matrix” to the Senate Resources Committee on April 16 (and a previous version to House Resources on April 1). It’s slide 19 of this deck. Past studies have shown that AK LNG’s “Phase 1” in-state pipeline would struggle to compete with the cost of imported LNG, and isn’t certain to beat it even with the governor’s 90% tax break. The promise of cheap gas for southcentral Alaskans depends on most of the pipeline’s cost being borne by consumers in Asia, particularly Japan, via the “Phase 2” export project.

But this breakeven matrix shows that competitive exports to Asia probably can’t happen without a subsidy from local public services via a very significant tax break. It also plays a dubious guessing game with AK LNG’s cost — $44 billion? $60 billion? Higher? — that demonstrates why Alaskans shouldn’t take Glenfarne seriously until they give us a real number.

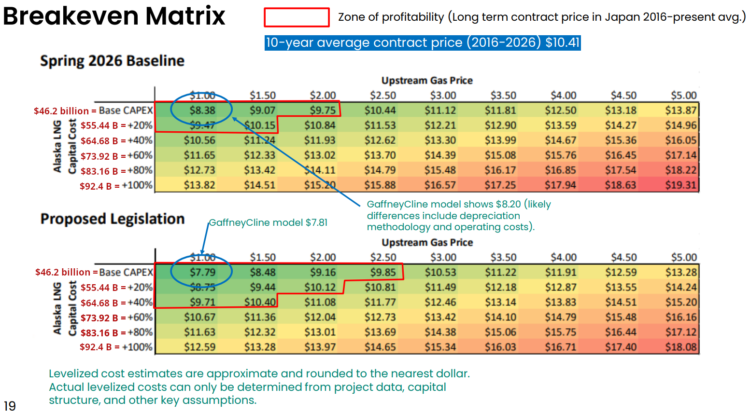

The Department of Revenue produced the underlying cost model, and initially presented it to House Resources on March 25 (see slide 34 in this deck). It shows the minimum price that AK LNG would need to demand for its gas in Asia, given a range of assumptions about:

- AK LNG’s construction cost, a.k.a capital expense (abbreviated “capex”). This is the vertical axis, ranging from $46.2 billion to $92.4 billion. I added in the corresponding dollar numbers in the graphic above.

- The price pipeline operators would need to pay for gas from the North Slope drillers, a.k.a. “upstream gas costs,” is on the horizontal axis, ranging from $1 to $5 per thousand cubic feet of gas.

The Department of Revenue produced two scenarios — the top matrix using status-quo property taxes, and the bottom matrix with the property tax break under the governor’s bills, which would exempt AK LNG from the normal assessment-based property tax system and instead take six cents per thousand cubic foot of gas moved through the pipeline – equivalent to a 90% tax break. Borough mayors in the pipeline area have found this insufficient for protecting their local taxpayers from AK LNG’s impact on public services and have not supported the bills.

Gaffney Cline added the red “Zones of Profitability” to the Department of Revenue’s chart, showing the range in which AK LNG’s minimum prices could be lower than Japan’s average LNG price over the past 10 years.

It’s obvious that the Zone of Profitability isn’t big. What’s less obvious is that with the real capital cost of AK LNG, the Zone of Profitability may not exist at all, unless the legislature gives AK LNG their tax break.

The Department of Revenue used $46.2 billion as the “base capex” in their model — an inflation adjustment of AK LNG’s official estimate of $44 billion, itself an inflation adjustment of a decade-old number. With 25-50% steel tariffs and rising costs for labor and equipment that have outstripped inflation, this old cost estimate is likely nowhere near accurate. Independent analysts Rapidan estimated a capital cost of $60 billion to $80 billion (roughly +40% to +80% of DOR’s baseline capex). Consulting engineer Lois Epstein thinks $66 billion is a good guess. If any of these estimates are closer to correct than the bogus number that the Department of Revenue knowingly used as a base, we should just cross out the first two rows of the matrix. Which means the profit zone is gone without the tax break. For AK LNG to get inside the profit zone with a gas contract that beats Japan’s average LNG cost of the past 10 years, it would need:

- The SB 280 / HB 381 tax break

- A capex under $64 billion, and

- Upstream gas costs under $1.50

These charts, with the likelihood of an AK LNG capex well over $46 billion, and the very high likelihood of cost overruns on top of that, show that we should stop betting on this project and turn our effort to real local energy solutions.

The big, ugly caveat is that, depending on what happens in the Strait of Hormuz, Japan’s 10-year average LNG price might be a thing of the past. But nobody today has a real idea what will happen. The global LNG market has had two huge eruptions of chaos (the wars in Ukraine and Iran) in the past five years — will this finally turn Asian utilities toward the stability and savings of renewables, or will they buy AK LNG’s security sales pitch and accept a price increase to double down on gas?

The geopolitical dice are still tumbling. But Alaska has better things to do than gamble on the roll.